by Hugo Brady

Ireland will elect a new government on February 25th to replace a discredited administration loathed by most Irish voters. At first sight, it seems unlikely the election will re-open the fundamentals of a bail-out agreed with fellow eurozone members and the IMF last November. The last act of Fianna Fáil, the main party in government since 1997, was to translate the terms of that deal into an initial set of tax hikes and further public spending cuts before leaving office. Nonetheless, the poll – Ireland’s most important for decades – marks a shift in hostility towards the bail-out and the EU in general which its partners would be foolish to ignore.

European benefactors might express shock that Irish attitudes towards the EU have worsened in the wake of the bail-out. To many EU leaders – including José Manuel Barroso, president of the European Commission – they are helping to rescue a country where politicians and regulators, through incompetence or worse, allowed bankers and developers to drive the economy to ruin using other people's money.* That view is correct but cloistered. It takes no account of the part played by the introduction of the euro itself – at a low interest rate hitherto unknown in Ireland – in inflating a runaway property boom. And Ireland's eurozone partners (along with Britain) do expect their money back at a profit, having – they hope – secured the common currency and the unwise investments of their own banks in the process.

Furthermore, the Irish version of events differs sharply from that of its partners, even when adjusted for the natural reluctance of any country to blame itself for its own woes. Most Irish people feel that the rest of the eurozone and European Central Bank imposed a bail-out that their country did not need (Ireland could have limped on until mid-2011 despite its astronomical debts) at an interest rate that it could not afford (5.8 per cent) in an ultimately futile attempt to contain a wider crisis. With a decade of austerity ahead and with no option to default, Ireland's voters gape in disbelief at new demands by continental politicians that it must now raise its low corporation tax rate. By the end of the year, Ireland will have lost 300,000 jobs from a labour market of 2.1 million. The country needs to retain foreign investment as a matter of economic survival.

Perhaps popular disenchantment was always unavoidable, but attitudes amongst Ireland's traditionally pro-EU elites have hardened too. Michael Noonan, the finance spokesperson of Fine Gael – an unambiguously pro-European Christian Democratic party and the one likely to form the bulk of the next government – has characterised the bail-out agreement as being forced on a punch-drunk government by lordly EU and IMF negotiators. Eamon Gilmore, the Irish Labour leader, whose party is likely to secure the finance portfolio in a new coalition, has also demanded a renegotiation of the terms of the agreement, saying the bail-out “clearly won't work. It provides no scope for the Irish economy to grow.”** Even Fianna Fáil – now under a far more effective leader in Micheál Martin, the former foreign affairs minster – will repudiate the agreement in time. And independent commentators in the media and respected think-tanks such as the Economic and Social Research Institute wonder aloud how Ireland will remain a euro country while extricating itself from its current situation.

Irish politics manages to fuse an Italian-style localism, ebullience and idiosyncrasy with the British parliamentary model. Ireland's politicians are usually uninterested in ideology, intensely sensitive to local concerns and poor at strategic thinking, one reason why they were unable to think past the boom. But popular Irish attitudes to national sovereignty closely mirror those of its nearest neighbour. In Britain, euroscepticism became a truly potent political force in the wake of the UK's forced exit from the European Exchange Rate Mechanism in 1992. Since then, pro-Europeans in Britain have dwindled to a small group of progressives. There is every reason to believe that the new generation of Irish politicians entering the scene at this election will view Ireland's difficulties with the euro as the ERM crisis for slow-learners. A flotilla of long-serving parliamentarians are bowing out of politics at this election in favour of younger candidates.

All of this matters doubly because – unlike Britain – Ireland has held a referendum on the future of European integration on average every four or five years since 1987. On the two occasions when Ireland has voted twice on the same treaty, Irish politicians were able to justify this by pointing to the fact that EU membership had been overwhelmingly beneficial to the country. Many voters now recall with bitterness how a desperate government assured them in October 2009 that a second vote on the Lisbon treaty would assist an imminent economic recovery. It will no longer be possible to be so categorial about Ireland's relationship with the EU, also bearing in mind that the country will shortly become a net contributor to the European budget. And the current uncertainty over the fate of the euro itself shows that the EU's constitutional future is by no means settled, as many had hoped when Lisbon was finally ratified.

Make no mistake: it is Ireland's politicians, not the EU, that will rightly be in the firing line on February 25th. But although Ireland may never again be able to serve as an unqualified European success story, the collapse of pro-European sentiment there could well come back to haunt the EU in future. In the 1990s, the IMF learned in Latin America that it is often wise to launch a charm offensive when a new government comes into power in a recipient country undergoing harsh economic adjustment. Ireland's eurozone partners and the ECB would be well advised to follow a similar approach by pre-empting the incoming government's demand for a renegotiation with an offer to lower the interest rate for loans needed to sustain the public finances. In time, the sparing of Irish blushes may save those of many others.

Hugo Brady is a senior research fellow at the Centre for European Reform

* http://www.irishtimes.com/newspaper/breaking/2011/0119/breaking52.html

** http://www.irishtimes.com/newspaper/ireland/2011/0106/1224286876810.html

Friday, January 28, 2011

Thursday, January 20, 2011

Can Greece be saved?

by Katinka Barysch

Will Greece have to restructure its debt? Among most West European economists and investors, this now seems to be a foregone conclusion. The Greeks themselves are not so sure. During a recent visit to Athens, none of the economists and politicians I spoke to thought that restructuring was inevitable or desirable. The Papandreou government looks determined. But to avoid default, Greece would need two things: economic growth and more help from its European neighbours.

Since Greece negotiated its €110 billion financial assistance package with the EU and the IMF last year, it has cut its government deficit by an impressive 6 per cent of GDP. The government has slashed public salaries and pensions, raised VAT and other taxes, and clamped down on ubiquitous tax evasion. Half a dozen big strikes and the occasional outbreak of street fighting notwithstanding, the Greeks have so far remained rather stoic in the face of this unprecedented belt tightening. Most realise that change is needed and hardship inevitable.

The other reason why Greeks have so far stayed calm is that the worst is yet to come. While civil servants, truckers and some other groups felt immediate pain, the population at large has not yet suffered unbearably. After 15 years of rising salaries, most Greeks can cope with an initial drop in income. Those who lose their job or business can usually rely on a tightly knit family network for support.

Greece, however, is not even half way through its deficit cutting programme. The total need for adjustment is 13-15 per cent of GDP. Cutting the first 20 or 30 per cent out of any budget is relatively easy – especially in a budget that contains as much flab as the Greek one. The public sector is overstaffed and, in many places, overpaid; pension entitlements are generous; although 60 per cent of the population lives in the capital, Greece has over 1,000 municipal administrations and 52 regional ones (a new law will cut those numbers by two-thirds); the country’s 150 public hospitals are accounting-free zones, which has contributed to spiralling healthcare costs; public enterprise such as the railways are black holes for government subsidies.

Once the most glaring inefficiencies have been removed, however, further reductions will get a lot harder. After the fat is gone, the government will have to cut bone. Papandreou needs to perform this operation at a time when the economy is in deep recession: by the end of this year, GDP will have contracted by as much as 10 per cent; unemployment is heading towards 15 per cent; among younger people, one in three is out of work; thousands of businesses are closing down every month.

Even if the government managed to stay on track with its plans for budget consolidation, public debt would continue to rise inexorably, to over 150 per cent of GDP by the end of this year. Greece will only stand a chance of generating the revenue needed to service such high debt if it returns to economic growth, and quickly.

The bad news is that in order to regain its competitiveness Greece will require an internal ‘devaluation’ – a fall in real wages relative to its trading partners. Such wage compression will dampen consumption and could even lead to damaging deflation. And it would not even address the deeper problem that Greece makes few things that people in other countries want to buy. Growth since the 1990s was led by consumption and fuelled by cheap foreign credit. To move to a more sustainable growth model, the country requires higher value-added industries and massive foreign investment. Neither will materialise without very thorough economic and institutional reforms. “In terms of institutions, infrastructure and corruption, Greece looks a bit like a third world country”, sighs one Greek fund manager based in London.

The somewhat better news is that Greece’s economy is so inefficient that a series of straightforward changes could kick-start an economic expansion. “In many sectors, our economy resembles Soviet central planning”, explains Yannis Stournaras, who runs the IOBE institute for economic and industrial research. “If we remove stifling regulation and bureaucracy, the economy’s dynamism will be unbound.” IOBE has calculated that liberalisation of the most heavily shackled sectors and professions would lift output by 10 per cent over four years, and probably more once dynamic, growth-boosting effects are taken into account.

Having implemented a first bout of budget-cutting policies, the Papandreou government is now setting to work on structural reforms. If things go according to plan, some 70 ‘closed shop’ professions, from lawyers to pharmacists and civil engineers, will lose many of their privileges and protections. Hiring and firing workers will get easier across the board. State enterprises will be restructured, downsized and sold off. Red tape for businesses will be cut. New incentives will boost investment in green energy, high-end tourism and other potential growth industries.

These plans are already creating fierce opposition from the highly organised groups that will be directly affected. The two main political parties, but Pasok in particular, rely on the trade unions and professional bodies for their core support. “Attacking the closed-shop professions means civil war within Pasok”, predicts Loukas Tsoukalis, head of Eliamep, a think-tank in Athens. Already, some Pasok MPs are grumbling that the reforms are now going too far, too fast. More strikes are inevitable.

Curiously, Greeks tend to sympathise with the plight of even the most molly-coddled public sector workers and privileged professionals. Faced with rising opposition within his own party and public restiveness, Papandreou’s resolve may yet falter.

Even if it does not, Papandreou will face the immovable object of his own state administration. Structural reforms will only boost growth if they are implemented swiftly and effectively. The chances of this happening are slim. A law going back to the post-dictatorship days makes the dismissal of civil servants illegal; even sacking public sector workers who do not strictly speaking enjoy civil service status is considered politically impossible. Each administration since the 1980s has added ‘its’ people to an already outsized state apparatus, often in return for votes and political support. The result is a public sector that is not only hopelessly bloated (roughly 800,000 out of a workforce of five million) but one that is infused with a sense of entitlement, rather than public duty.

Until and unless growth resumes, Greece will struggle to cope with its stifling debt burden. Greeks hope that the EU will step in again to tide the country over until the economy recovers. Many hope that Germany will drop its opposition to joint eurozone bonds, which would help to lower the interest rate at which Greece borrows and refinances its debt. Others suggest that the EU could ‘front-load’ regional aid to boost Greek investment over the next couple of years.

If no further EU help is forthcoming, or the debt burden proves unsustainable, Greece may yet be forced to negotiate a rescheduling or restructuring with its creditors. Since Greek politicians are loath to consider the default option publicly, this would come as a shock to many ordinary Greeks. Many might be directly affected if (as seems likely) a public debt restructuring triggers a crisis within the Greek banking sector and social security funds. Most Greeks would consider default as a terminal blow to the country’s standing inside the EU.

Greeks have traditionally been very pro-EU, and not only because the country has been one of the biggest recipients of EU structural funds since the 1980s. All political parties, with the exception of the Communists, are in favour of more European integration. Remarkably few Greeks have so far blamed the EU (or the IMF for that matter) for the hardship they are going through – although Germans, and Chancellor Merkel in particular, are deeply unpopular for dithering over the bail-out and lecturing the Greeks about their allegedly lazy and lavish ways.

If Greece was forced to restructure, politicians and public opinion could quickly turn against the EU. “The Greeks would say: We’ve been through pain and austerity, and now you drop us”, predicts Panagiotis Ioakeimidis, professor at Athens university and an EU specialist. Some Greeks fear that after default, Greece’s membership in the euro, and the EU itself, may be questioned. That is why the Greeks will hold out fiercely against any pressure to consider restructuring.

Katinka Barysch is deputy director of the Centre for European Reform

Will Greece have to restructure its debt? Among most West European economists and investors, this now seems to be a foregone conclusion. The Greeks themselves are not so sure. During a recent visit to Athens, none of the economists and politicians I spoke to thought that restructuring was inevitable or desirable. The Papandreou government looks determined. But to avoid default, Greece would need two things: economic growth and more help from its European neighbours.

Since Greece negotiated its €110 billion financial assistance package with the EU and the IMF last year, it has cut its government deficit by an impressive 6 per cent of GDP. The government has slashed public salaries and pensions, raised VAT and other taxes, and clamped down on ubiquitous tax evasion. Half a dozen big strikes and the occasional outbreak of street fighting notwithstanding, the Greeks have so far remained rather stoic in the face of this unprecedented belt tightening. Most realise that change is needed and hardship inevitable.

The other reason why Greeks have so far stayed calm is that the worst is yet to come. While civil servants, truckers and some other groups felt immediate pain, the population at large has not yet suffered unbearably. After 15 years of rising salaries, most Greeks can cope with an initial drop in income. Those who lose their job or business can usually rely on a tightly knit family network for support.

Greece, however, is not even half way through its deficit cutting programme. The total need for adjustment is 13-15 per cent of GDP. Cutting the first 20 or 30 per cent out of any budget is relatively easy – especially in a budget that contains as much flab as the Greek one. The public sector is overstaffed and, in many places, overpaid; pension entitlements are generous; although 60 per cent of the population lives in the capital, Greece has over 1,000 municipal administrations and 52 regional ones (a new law will cut those numbers by two-thirds); the country’s 150 public hospitals are accounting-free zones, which has contributed to spiralling healthcare costs; public enterprise such as the railways are black holes for government subsidies.

Once the most glaring inefficiencies have been removed, however, further reductions will get a lot harder. After the fat is gone, the government will have to cut bone. Papandreou needs to perform this operation at a time when the economy is in deep recession: by the end of this year, GDP will have contracted by as much as 10 per cent; unemployment is heading towards 15 per cent; among younger people, one in three is out of work; thousands of businesses are closing down every month.

Even if the government managed to stay on track with its plans for budget consolidation, public debt would continue to rise inexorably, to over 150 per cent of GDP by the end of this year. Greece will only stand a chance of generating the revenue needed to service such high debt if it returns to economic growth, and quickly.

The bad news is that in order to regain its competitiveness Greece will require an internal ‘devaluation’ – a fall in real wages relative to its trading partners. Such wage compression will dampen consumption and could even lead to damaging deflation. And it would not even address the deeper problem that Greece makes few things that people in other countries want to buy. Growth since the 1990s was led by consumption and fuelled by cheap foreign credit. To move to a more sustainable growth model, the country requires higher value-added industries and massive foreign investment. Neither will materialise without very thorough economic and institutional reforms. “In terms of institutions, infrastructure and corruption, Greece looks a bit like a third world country”, sighs one Greek fund manager based in London.

The somewhat better news is that Greece’s economy is so inefficient that a series of straightforward changes could kick-start an economic expansion. “In many sectors, our economy resembles Soviet central planning”, explains Yannis Stournaras, who runs the IOBE institute for economic and industrial research. “If we remove stifling regulation and bureaucracy, the economy’s dynamism will be unbound.” IOBE has calculated that liberalisation of the most heavily shackled sectors and professions would lift output by 10 per cent over four years, and probably more once dynamic, growth-boosting effects are taken into account.

Having implemented a first bout of budget-cutting policies, the Papandreou government is now setting to work on structural reforms. If things go according to plan, some 70 ‘closed shop’ professions, from lawyers to pharmacists and civil engineers, will lose many of their privileges and protections. Hiring and firing workers will get easier across the board. State enterprises will be restructured, downsized and sold off. Red tape for businesses will be cut. New incentives will boost investment in green energy, high-end tourism and other potential growth industries.

These plans are already creating fierce opposition from the highly organised groups that will be directly affected. The two main political parties, but Pasok in particular, rely on the trade unions and professional bodies for their core support. “Attacking the closed-shop professions means civil war within Pasok”, predicts Loukas Tsoukalis, head of Eliamep, a think-tank in Athens. Already, some Pasok MPs are grumbling that the reforms are now going too far, too fast. More strikes are inevitable.

Curiously, Greeks tend to sympathise with the plight of even the most molly-coddled public sector workers and privileged professionals. Faced with rising opposition within his own party and public restiveness, Papandreou’s resolve may yet falter.

Even if it does not, Papandreou will face the immovable object of his own state administration. Structural reforms will only boost growth if they are implemented swiftly and effectively. The chances of this happening are slim. A law going back to the post-dictatorship days makes the dismissal of civil servants illegal; even sacking public sector workers who do not strictly speaking enjoy civil service status is considered politically impossible. Each administration since the 1980s has added ‘its’ people to an already outsized state apparatus, often in return for votes and political support. The result is a public sector that is not only hopelessly bloated (roughly 800,000 out of a workforce of five million) but one that is infused with a sense of entitlement, rather than public duty.

Until and unless growth resumes, Greece will struggle to cope with its stifling debt burden. Greeks hope that the EU will step in again to tide the country over until the economy recovers. Many hope that Germany will drop its opposition to joint eurozone bonds, which would help to lower the interest rate at which Greece borrows and refinances its debt. Others suggest that the EU could ‘front-load’ regional aid to boost Greek investment over the next couple of years.

If no further EU help is forthcoming, or the debt burden proves unsustainable, Greece may yet be forced to negotiate a rescheduling or restructuring with its creditors. Since Greek politicians are loath to consider the default option publicly, this would come as a shock to many ordinary Greeks. Many might be directly affected if (as seems likely) a public debt restructuring triggers a crisis within the Greek banking sector and social security funds. Most Greeks would consider default as a terminal blow to the country’s standing inside the EU.

Greeks have traditionally been very pro-EU, and not only because the country has been one of the biggest recipients of EU structural funds since the 1980s. All political parties, with the exception of the Communists, are in favour of more European integration. Remarkably few Greeks have so far blamed the EU (or the IMF for that matter) for the hardship they are going through – although Germans, and Chancellor Merkel in particular, are deeply unpopular for dithering over the bail-out and lecturing the Greeks about their allegedly lazy and lavish ways.

If Greece was forced to restructure, politicians and public opinion could quickly turn against the EU. “The Greeks would say: We’ve been through pain and austerity, and now you drop us”, predicts Panagiotis Ioakeimidis, professor at Athens university and an EU specialist. Some Greeks fear that after default, Greece’s membership in the euro, and the EU itself, may be questioned. That is why the Greeks will hold out fiercely against any pressure to consider restructuring.

Katinka Barysch is deputy director of the Centre for European Reform

Monday, January 17, 2011

Euro crisis: In defence of investors

by Simon Tilford

The eurozone’s fiscal position is better than the US and UK, and the crisis-hit members of the currency union are doing more to strengthen their public finances than either of these countries. So why are borrowing costs so much higher for countries in the eurozone periphery than for Britain and America? Portugal and Greece have lower public deficits than the US, so why do investors fear for their solvency, but not that of the US?

These questions are being put with increasing frustration by eurozone economists, from both the public and private sectors, as well as by policy-makers such as Juergen Stark at the European Central Bank. The inference is that investors are judging countries by different standards. Why else would investors continue to lend to the likes of the ‘profligate’ US and UK, but punish countries whose fundamentals are sounder? Such irrational behaviour by investors, it is argued, is unfairly derailing the hard work being done by governments in the eurozone. Are such frustrations justified?

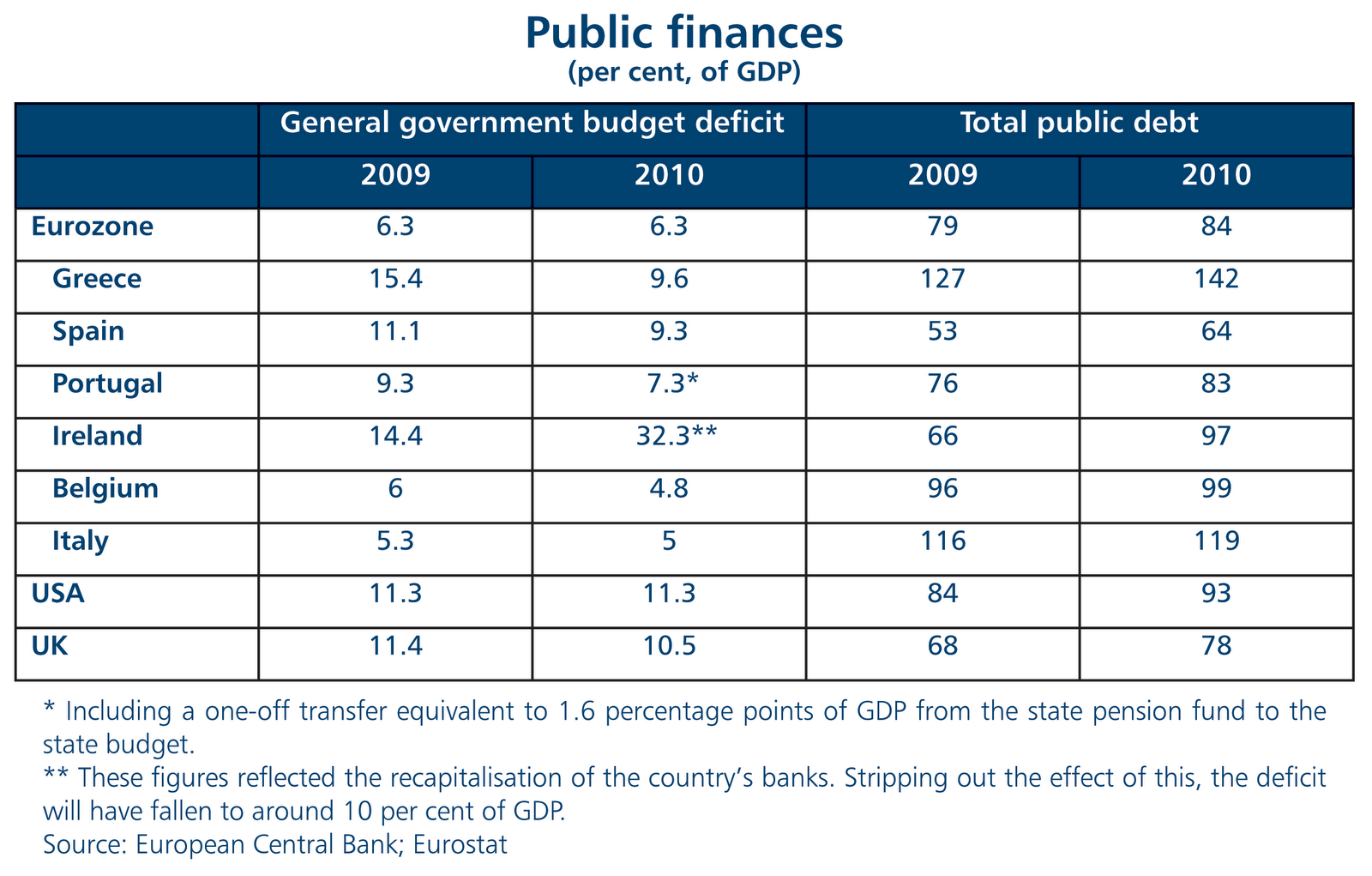

Investors do appear, superficially at least, to be harsh in their attitude towards the eurozone. As Table 1 below shows, the eurozone's aggregate budget deficit is lower than in the UK or the US; its aggregate debt is marginally higher than in the UK, but lower than in the US; and in struggling Spain, public debt is lower than in both the US and the UK.

But anything more than a very superficial analysis shows why investors are right to be concerned about the eurozone. First, there is no federal eurozone budget, so the aggregate budget deficit is only of so much interest to investors. Second, it is countries’ ability to service their debts going forward that determines the risk premium demanded by investors, and to a large extent this depends on their economic growth prospects. While the crisis-hit eurozone economies have made more progress in reducing their borrowing than did either the UK or US, this has been at the cost of economic stagnation. Third, sovereign investors are not just concerned about public debt, but levels of private indebtedness too. They fear that if economic growth remains very weak, governments will end up being liable for some of the private debt.

Eurozone economic growth was a respectable enough 1.7 per cent in 2010 (see Table 2). This was well below the US, but about the same as the UK. However, the eurozone figures masked huge differences. Germany, which accounts for a third of the currency union’s GDP, expanded by 3.6 per cent, whereas Greece’s economy contracted steeply and a number of others barely grew. Stripping out Germany, eurozone economic growth was actually just 1 per cent in 2010. Indeed, the eurozone is still a long way from returning to its pre-crisis level of economic activity: in the third quarter of 2010 eurozone GDP was still 3.2 per cent lower than in the first quarter of 2008. This was better than the UK but far worse than the US, whose economy was almost 2 per cent larger in the third quarter of 2010 than at the outset of the downturn. Not only is real GDP in some of the struggling economies still way below their pre-crisis peaks, but there is little chance of them returning to pre-crisis levels any time soon.

Are investors right to be so pessimistic about the economic growth prospects of the struggling member-states? Yes, because their prospects of economic recovery rest on a strong rise in exports, but the principal way of bringing this about – real devaluation within the eurozone – threatens economic stagnation and rising debt burdens. Because of their membership of the currency union they cannot devalue their currencies, so must reduce their wages and prices relative to their eurozone counterparts. The problem is that this will depress income and lead to deflationary pressures. This, in turn, will make it hard to bring down deficits on a sustained basis (irrespective of how wrenching fiscal austerity is), and will inflate debt servicing costs. A strategy of deflating back to competitiveness might be do-able for an economy with little or no debt, but for the crisis-hit eurozone economies it is high-risk.

Portugal has combined public and private debt of around 320 per cent of GDP. The Portuguese central bank expects real GDP to contract by 1.3 per cent in 2011, while inflation is unlikely to be much more than 1.5 per cent. This implies stagnant nominal GDP (growth in real GDP and inflation). There was much fanfare this week when Portugal successfully sold a modest quantity of government bonds at a yield of 6.7 per cent, but this is a ruinous rate of interest for an economy with Portugal’s prospects. The picture is somewhat better in Spain (hence investors are demanding less of a premium to lend to the Spanish government). Ireland has managed to execute a major internal devaluation within the eurozone, but at the cost of an unprecedented decline in its nominal GDP and an explosion in the country’s debt burden. With Greece’s stock of public debt at 140 per cent of GDP and its economy contracting rapidly, it is hardly surprising that investors have little appetite for Greek bonds.

But what of the structural reforms being pushed through by these countries? Why are investors not taking more account of these? There is no doubt that Spain, Greece and Portugal are now introducing long overdue reforms of their labour markets. These reforms are obviously welcome, and in the long-term should help to boost productivity growth. But a little perspective is needed. Notwithstanding modest moves to free up the markets for professional services in Greece and Portugal, there is little sign of an aggressive drive to open-up these countries’ domestic sectors to more competition. And without such aggressive liberalisation, productivity growth will remain anaemic. Moreover, there are legitimate doubts over the ability of governments to push through an ongoing programme of unpopular reforms when their economies are caught in a cycle of weak economic growth and rising debt burdens. There needs to be light at the end of the tunnel.

What of debt dynamics in the UK and US? Are they not even worse? Both face daunting fiscal challenges and high levels of household indebtedness. And the US at least relies on foreign investors to finance a significant chunk of its budget deficit. But there are several good reasons for investors to be more relaxed about the solvency of the US (and to a somewhat lesser degree, the UK) than the crisis-hit members of the currency union. Unlike their eurozone counterparts, who must rely on deflation to rebalance their economies, the US and UK can rely on currency depreciation to facilitate the necessary adjustment and boost exports. Currency depreciation and very activist central banks in these two countries also ensures that deflation is unlikely to be problem. In addition, both countries have far more flexible product and labour markets than the southern European countries.

In short, the reason why the US and UK can borrow at much lower rates of interest than the similarly indebted members of the eurozone is that the obstacles to economic growth are lower in Britain and America and threat of deflation and mounting social tensions much less acute. Of course, investors could yet take fright if economic recovery in the two countries peters out and their fiscal deficits remain too high. The UK, more than the US, could certainly find itself in this position. But in such a situation, sterling would fall, encouraged no doubt by a further bout of so-called quantitative easing by the Bank of England. And fortunately for the British government, it largely relies on domestic institutional investors to fund its fiscal deficit; this is not so in the case of the currency union’s strugglers.

Unsustainable macroeconomic policies explain investors’ flight from the sovereign debt of the crisis-hit eurozone economies. Until the eurozone demonstrates how the currency union’s peripheral economies are going to avoid stagnation and debt traps, it will be rational for investors to give their sovereign debt a wide berth.

Simon Tilford is chief economist at the Centre for European Reform.

The eurozone’s fiscal position is better than the US and UK, and the crisis-hit members of the currency union are doing more to strengthen their public finances than either of these countries. So why are borrowing costs so much higher for countries in the eurozone periphery than for Britain and America? Portugal and Greece have lower public deficits than the US, so why do investors fear for their solvency, but not that of the US?

These questions are being put with increasing frustration by eurozone economists, from both the public and private sectors, as well as by policy-makers such as Juergen Stark at the European Central Bank. The inference is that investors are judging countries by different standards. Why else would investors continue to lend to the likes of the ‘profligate’ US and UK, but punish countries whose fundamentals are sounder? Such irrational behaviour by investors, it is argued, is unfairly derailing the hard work being done by governments in the eurozone. Are such frustrations justified?

Investors do appear, superficially at least, to be harsh in their attitude towards the eurozone. As Table 1 below shows, the eurozone's aggregate budget deficit is lower than in the UK or the US; its aggregate debt is marginally higher than in the UK, but lower than in the US; and in struggling Spain, public debt is lower than in both the US and the UK.

But anything more than a very superficial analysis shows why investors are right to be concerned about the eurozone. First, there is no federal eurozone budget, so the aggregate budget deficit is only of so much interest to investors. Second, it is countries’ ability to service their debts going forward that determines the risk premium demanded by investors, and to a large extent this depends on their economic growth prospects. While the crisis-hit eurozone economies have made more progress in reducing their borrowing than did either the UK or US, this has been at the cost of economic stagnation. Third, sovereign investors are not just concerned about public debt, but levels of private indebtedness too. They fear that if economic growth remains very weak, governments will end up being liable for some of the private debt.

Eurozone economic growth was a respectable enough 1.7 per cent in 2010 (see Table 2). This was well below the US, but about the same as the UK. However, the eurozone figures masked huge differences. Germany, which accounts for a third of the currency union’s GDP, expanded by 3.6 per cent, whereas Greece’s economy contracted steeply and a number of others barely grew. Stripping out Germany, eurozone economic growth was actually just 1 per cent in 2010. Indeed, the eurozone is still a long way from returning to its pre-crisis level of economic activity: in the third quarter of 2010 eurozone GDP was still 3.2 per cent lower than in the first quarter of 2008. This was better than the UK but far worse than the US, whose economy was almost 2 per cent larger in the third quarter of 2010 than at the outset of the downturn. Not only is real GDP in some of the struggling economies still way below their pre-crisis peaks, but there is little chance of them returning to pre-crisis levels any time soon.

Are investors right to be so pessimistic about the economic growth prospects of the struggling member-states? Yes, because their prospects of economic recovery rest on a strong rise in exports, but the principal way of bringing this about – real devaluation within the eurozone – threatens economic stagnation and rising debt burdens. Because of their membership of the currency union they cannot devalue their currencies, so must reduce their wages and prices relative to their eurozone counterparts. The problem is that this will depress income and lead to deflationary pressures. This, in turn, will make it hard to bring down deficits on a sustained basis (irrespective of how wrenching fiscal austerity is), and will inflate debt servicing costs. A strategy of deflating back to competitiveness might be do-able for an economy with little or no debt, but for the crisis-hit eurozone economies it is high-risk.

Portugal has combined public and private debt of around 320 per cent of GDP. The Portuguese central bank expects real GDP to contract by 1.3 per cent in 2011, while inflation is unlikely to be much more than 1.5 per cent. This implies stagnant nominal GDP (growth in real GDP and inflation). There was much fanfare this week when Portugal successfully sold a modest quantity of government bonds at a yield of 6.7 per cent, but this is a ruinous rate of interest for an economy with Portugal’s prospects. The picture is somewhat better in Spain (hence investors are demanding less of a premium to lend to the Spanish government). Ireland has managed to execute a major internal devaluation within the eurozone, but at the cost of an unprecedented decline in its nominal GDP and an explosion in the country’s debt burden. With Greece’s stock of public debt at 140 per cent of GDP and its economy contracting rapidly, it is hardly surprising that investors have little appetite for Greek bonds.

But what of the structural reforms being pushed through by these countries? Why are investors not taking more account of these? There is no doubt that Spain, Greece and Portugal are now introducing long overdue reforms of their labour markets. These reforms are obviously welcome, and in the long-term should help to boost productivity growth. But a little perspective is needed. Notwithstanding modest moves to free up the markets for professional services in Greece and Portugal, there is little sign of an aggressive drive to open-up these countries’ domestic sectors to more competition. And without such aggressive liberalisation, productivity growth will remain anaemic. Moreover, there are legitimate doubts over the ability of governments to push through an ongoing programme of unpopular reforms when their economies are caught in a cycle of weak economic growth and rising debt burdens. There needs to be light at the end of the tunnel.

What of debt dynamics in the UK and US? Are they not even worse? Both face daunting fiscal challenges and high levels of household indebtedness. And the US at least relies on foreign investors to finance a significant chunk of its budget deficit. But there are several good reasons for investors to be more relaxed about the solvency of the US (and to a somewhat lesser degree, the UK) than the crisis-hit members of the currency union. Unlike their eurozone counterparts, who must rely on deflation to rebalance their economies, the US and UK can rely on currency depreciation to facilitate the necessary adjustment and boost exports. Currency depreciation and very activist central banks in these two countries also ensures that deflation is unlikely to be problem. In addition, both countries have far more flexible product and labour markets than the southern European countries.

In short, the reason why the US and UK can borrow at much lower rates of interest than the similarly indebted members of the eurozone is that the obstacles to economic growth are lower in Britain and America and threat of deflation and mounting social tensions much less acute. Of course, investors could yet take fright if economic recovery in the two countries peters out and their fiscal deficits remain too high. The UK, more than the US, could certainly find itself in this position. But in such a situation, sterling would fall, encouraged no doubt by a further bout of so-called quantitative easing by the Bank of England. And fortunately for the British government, it largely relies on domestic institutional investors to fund its fiscal deficit; this is not so in the case of the currency union’s strugglers.

Unsustainable macroeconomic policies explain investors’ flight from the sovereign debt of the crisis-hit eurozone economies. Until the eurozone demonstrates how the currency union’s peripheral economies are going to avoid stagnation and debt traps, it will be rational for investors to give their sovereign debt a wide berth.

Simon Tilford is chief economist at the Centre for European Reform.

Thursday, January 13, 2011

Reflections on Tommaso Padoa-Schioppa and the euro

By Charles Grant

At the end of last year, Europe lost Tommaso Padoa-Schioppa, an eminent central banker and economist, and one of the founding fathers of the euro. As EU leaders struggle to cope with the continuing euro crisis, they would do well do ponder some of Padoa-Schioppa’s insights on the economics of monetary union.

Following Greece and Ireland, Portugal may soon require a rescue from its fellow eurozone members. With the benefit of hindsight it is only too evident that the euro has suffered from design flaws, and that European leaders have mismanaged the currency. Too many countries joined the euro before they were ready. Fiscal discipline has been too lax, though new rules will make it harder for governments to over-borrow. Some eurozone governments did far too little to promote structural reform, and have therefore suffered from inflexible economies and poor productivity; in 2010, Greece, Portugal and Spain belatedly implemented some structural reforms. The penal rates of interest at which Greece, Ireland and Portugal have had to borrow have revealed the need for a bail-out mechanism and a procedure for ensuring the relatively orderly restructuring of sovereign debt (both are on their way). The behaviour of many banks – and not only in Ireland and Spain – has shown that the tighter system of pan-European financial regulation now being put together is sorely needed.

The statesmen who designed the euro have been criticised for putting politics ahead of economics: motivated by the desire to promote European unification, they ignored the economics – or assumed that once the project got underway, the necessary rules for economic governance would somehow fall into place. There is truth in that criticism, but many people have forgotten that economics did play a role in the birth of the euro.

In 1987, Padoa-Schioppa wrote a report explaining that the exchange rate mechanism (ERM) – which limited fluctuations among many European currencies – could not survive the removal of exchange controls that was agreed in that year. He wrote: “The complete liberalisation of capital movements is inconsistent with the present combination of exchange rate stability and the considerable national autonomy in the conduct of monetary policy.” He also argued that the end of the ERM and the return of currency instability would endanger the single market.

This report convinced Jacques Delors, the then president of the European Commission, and other leaders, that moving towards economic and monetary union (EMU) was urgent. So in 1988 EU leaders tasked a committee – which had Delors as its chairman and Padoa-Schioppa as its joint rapporteur – with drawing up plans for EMU. Delors and Padoa-Schioppa got most of what they wanted, though the Germans forced them – reluctantly – to accept the principle of binding rules on budget deficits. Most of the Delors committee’s report ended up in the Maastricht treaty in 1991. The ERM would not have survived the currency crises of 1992 and 1993 – when the capital markets nearly tore it apart – without the momentum towards monetary union.

In 2000, when a member of the executive board of the European Central Bank (ECB), Padoa-Schioppa wrote a brilliant essay for the CER, ‘Europe’s new economic policy constitution’. He complained about the weakness of the arrangements for co-ordinating national fiscal policies, arguing that if the eurozone could develop its own fiscal stance, the ECB could better manage monetary policy and more easily keep down interest rates. He also warned that the eurozone would not work well unless governments made labour markets more flexible; doing so would facilitate “higher non-inflationary growth. This in turn would increase fiscal sustainability on both the income and expenditure sides of the budget.”

Padoa-Schioppa’s death has deprived Europe of a courteous public servant who was utterly committed to European unity. Many of his insights have long-lasting relevance, and not only on labour markets. The EU’s new procedure for a ‘European semester’, involving peer review of national budgets, is a step towards the fiscal co-ordination he called for. Above all, Padoa-Schioppa understood the relevance of the euro to the single market. If the euro disappeared, giving way to competitive devaluations and wild currency swings, there is a serious risk that member-states would either impose tariffs against each other or resort to hidden forms of protectionism. Alternatives to the euro would not look pretty.

Like Padoa-Schioppa, the CER has long argued that a healthy eurozone requires much more thorough economic reform. In the flurry of regulatory and institutional reforms now underway, one of the most serious underlying problems in the eurozone is not being addressed. This is the growing gap in competitiveness between the eurozone’s core in northern Europe, and the southern states. This has led to large current account imbalances within the eurozone, and these have left the southern countries struggling to grow and to pay back debts.

One economist who foresaw that these imbalances would be a problem was the CER’s Simon Tilford, whose remarkably prescient CER report, ‘Will the eurozone crack?’, was published in September 2006. Simon wrote: “The core problem is that membership seems to have reduced pressure on governments to undertake the reforms needed to ensure the currency union is a success. Freed from the risk of a currency crisis and higher debt service costs, Italy [and the other southern countries have] done little to strengthen public finances, make labour markets more flexible or introduce more competition. The result has been declining productivity, inflation above the eurozone average and a sharp decline in competitiveness relative to other members of the eurozone. Unable to devalue its currency, Italy now risks getting caught in a vicious circle of very slow economic growth and rising debt.”

Simon predicted, rightly, that the markets’ inability to distinguish between the debts of different eurozone countries would lead to a damaging lack of fiscal discipline. He also pointed out that Germany’s “de facto competitive devaluation”, through low wage growth, would exacerbate eurozone imbalances. “While this has massively boosted the country’s competitiveness and its exports, it has depressed consumption and investment, causing the country’s trade and current account surpluses to balloon. An economy as big as Germany’s cannot depend indefinitely on exports to drive real GDP growth, without imposing intolerable pressures on other members of EMU.” On the other hand, “a German economy growing under its own steam would boost demand across the eurozone, cushioning the impact of structural reforms, and crucially, make it easier for other member-states to restore their competitiveness without forcing their economies into a prolonged recession.”

One reason to be gloomy about the euro is the intellectual rift that divides European leaders. It is as though the doctors examining the patient do not agree on the diagnosis or the medicine required. At the risk of some generalisation, leaders from Germanic and Nordic cultures believe that stricter fiscal discipline and structural reform will suffice to cure the patient. Those from Latin and Anglo-Saxon cultures think that medicine is necessary but not sufficient: they also focus on the imbalances and the need for the core countries with external surpluses to generate demand in the eurozone.

Despite all the problems, I expect the euro to survive, because the political will of EU leaders – including those in Germany – to do what it takes to preserve the currency remains strong. But political will on its own will not suffice; Europe’s leaders must also listen to economists if they want to put the euro on a truly sustainable footing.

Charles Grant is director of the Centre for European Reform

At the end of last year, Europe lost Tommaso Padoa-Schioppa, an eminent central banker and economist, and one of the founding fathers of the euro. As EU leaders struggle to cope with the continuing euro crisis, they would do well do ponder some of Padoa-Schioppa’s insights on the economics of monetary union.

Following Greece and Ireland, Portugal may soon require a rescue from its fellow eurozone members. With the benefit of hindsight it is only too evident that the euro has suffered from design flaws, and that European leaders have mismanaged the currency. Too many countries joined the euro before they were ready. Fiscal discipline has been too lax, though new rules will make it harder for governments to over-borrow. Some eurozone governments did far too little to promote structural reform, and have therefore suffered from inflexible economies and poor productivity; in 2010, Greece, Portugal and Spain belatedly implemented some structural reforms. The penal rates of interest at which Greece, Ireland and Portugal have had to borrow have revealed the need for a bail-out mechanism and a procedure for ensuring the relatively orderly restructuring of sovereign debt (both are on their way). The behaviour of many banks – and not only in Ireland and Spain – has shown that the tighter system of pan-European financial regulation now being put together is sorely needed.

The statesmen who designed the euro have been criticised for putting politics ahead of economics: motivated by the desire to promote European unification, they ignored the economics – or assumed that once the project got underway, the necessary rules for economic governance would somehow fall into place. There is truth in that criticism, but many people have forgotten that economics did play a role in the birth of the euro.

In 1987, Padoa-Schioppa wrote a report explaining that the exchange rate mechanism (ERM) – which limited fluctuations among many European currencies – could not survive the removal of exchange controls that was agreed in that year. He wrote: “The complete liberalisation of capital movements is inconsistent with the present combination of exchange rate stability and the considerable national autonomy in the conduct of monetary policy.” He also argued that the end of the ERM and the return of currency instability would endanger the single market.

This report convinced Jacques Delors, the then president of the European Commission, and other leaders, that moving towards economic and monetary union (EMU) was urgent. So in 1988 EU leaders tasked a committee – which had Delors as its chairman and Padoa-Schioppa as its joint rapporteur – with drawing up plans for EMU. Delors and Padoa-Schioppa got most of what they wanted, though the Germans forced them – reluctantly – to accept the principle of binding rules on budget deficits. Most of the Delors committee’s report ended up in the Maastricht treaty in 1991. The ERM would not have survived the currency crises of 1992 and 1993 – when the capital markets nearly tore it apart – without the momentum towards monetary union.

In 2000, when a member of the executive board of the European Central Bank (ECB), Padoa-Schioppa wrote a brilliant essay for the CER, ‘Europe’s new economic policy constitution’. He complained about the weakness of the arrangements for co-ordinating national fiscal policies, arguing that if the eurozone could develop its own fiscal stance, the ECB could better manage monetary policy and more easily keep down interest rates. He also warned that the eurozone would not work well unless governments made labour markets more flexible; doing so would facilitate “higher non-inflationary growth. This in turn would increase fiscal sustainability on both the income and expenditure sides of the budget.”

Padoa-Schioppa’s death has deprived Europe of a courteous public servant who was utterly committed to European unity. Many of his insights have long-lasting relevance, and not only on labour markets. The EU’s new procedure for a ‘European semester’, involving peer review of national budgets, is a step towards the fiscal co-ordination he called for. Above all, Padoa-Schioppa understood the relevance of the euro to the single market. If the euro disappeared, giving way to competitive devaluations and wild currency swings, there is a serious risk that member-states would either impose tariffs against each other or resort to hidden forms of protectionism. Alternatives to the euro would not look pretty.

Like Padoa-Schioppa, the CER has long argued that a healthy eurozone requires much more thorough economic reform. In the flurry of regulatory and institutional reforms now underway, one of the most serious underlying problems in the eurozone is not being addressed. This is the growing gap in competitiveness between the eurozone’s core in northern Europe, and the southern states. This has led to large current account imbalances within the eurozone, and these have left the southern countries struggling to grow and to pay back debts.

One economist who foresaw that these imbalances would be a problem was the CER’s Simon Tilford, whose remarkably prescient CER report, ‘Will the eurozone crack?’, was published in September 2006. Simon wrote: “The core problem is that membership seems to have reduced pressure on governments to undertake the reforms needed to ensure the currency union is a success. Freed from the risk of a currency crisis and higher debt service costs, Italy [and the other southern countries have] done little to strengthen public finances, make labour markets more flexible or introduce more competition. The result has been declining productivity, inflation above the eurozone average and a sharp decline in competitiveness relative to other members of the eurozone. Unable to devalue its currency, Italy now risks getting caught in a vicious circle of very slow economic growth and rising debt.”

Simon predicted, rightly, that the markets’ inability to distinguish between the debts of different eurozone countries would lead to a damaging lack of fiscal discipline. He also pointed out that Germany’s “de facto competitive devaluation”, through low wage growth, would exacerbate eurozone imbalances. “While this has massively boosted the country’s competitiveness and its exports, it has depressed consumption and investment, causing the country’s trade and current account surpluses to balloon. An economy as big as Germany’s cannot depend indefinitely on exports to drive real GDP growth, without imposing intolerable pressures on other members of EMU.” On the other hand, “a German economy growing under its own steam would boost demand across the eurozone, cushioning the impact of structural reforms, and crucially, make it easier for other member-states to restore their competitiveness without forcing their economies into a prolonged recession.”

One reason to be gloomy about the euro is the intellectual rift that divides European leaders. It is as though the doctors examining the patient do not agree on the diagnosis or the medicine required. At the risk of some generalisation, leaders from Germanic and Nordic cultures believe that stricter fiscal discipline and structural reform will suffice to cure the patient. Those from Latin and Anglo-Saxon cultures think that medicine is necessary but not sufficient: they also focus on the imbalances and the need for the core countries with external surpluses to generate demand in the eurozone.

Despite all the problems, I expect the euro to survive, because the political will of EU leaders – including those in Germany – to do what it takes to preserve the currency remains strong. But political will on its own will not suffice; Europe’s leaders must also listen to economists if they want to put the euro on a truly sustainable footing.

Charles Grant is director of the Centre for European Reform

Subscribe to:

Comments (Atom)